Why Reverse Mortgages Are Getting Attention

Reverse mortgages are being talked about more than ever right now. Rising interest rates, higher living costs, and the reality that many homeowners are “house rich but cash poor” have pushed this product into the spotlight, especially for retirees.

On the surface, it sounds simple: access the equity in your home without making monthly payments, but like many things in real estate and finance, the reality is more complex.

What a Reverse Mortgage Actually Is

A reverse mortgage allows homeowners (typically 55+) to borrow against the value of their home without making regular payments. Instead, interest is added to the loan balance over time, and the loan is repaid when the home is sold or the owner moves out or passes away.

In other words, you are spending your home equity now, and settling the bill later.

Why They’re Becoming More Common

This product is gaining traction for understandable reasons. Many homeowners have built significant equity over the past decade, while retirement income has not kept pace with inflation. Traditional lending can be harder to qualify for later in life, and many people want to remain in their homes as long as possible. For some, a reverse mortgage feels like a practical solution.The Part Most People Don’t Fully Understand

Reverse mortgages are not free money. Because there are no monthly payments, the interest compounds over time. That means the loan grows, and your remaining equity shrinks. And it doesn’t shrink slowly — it accelerates rapidly.

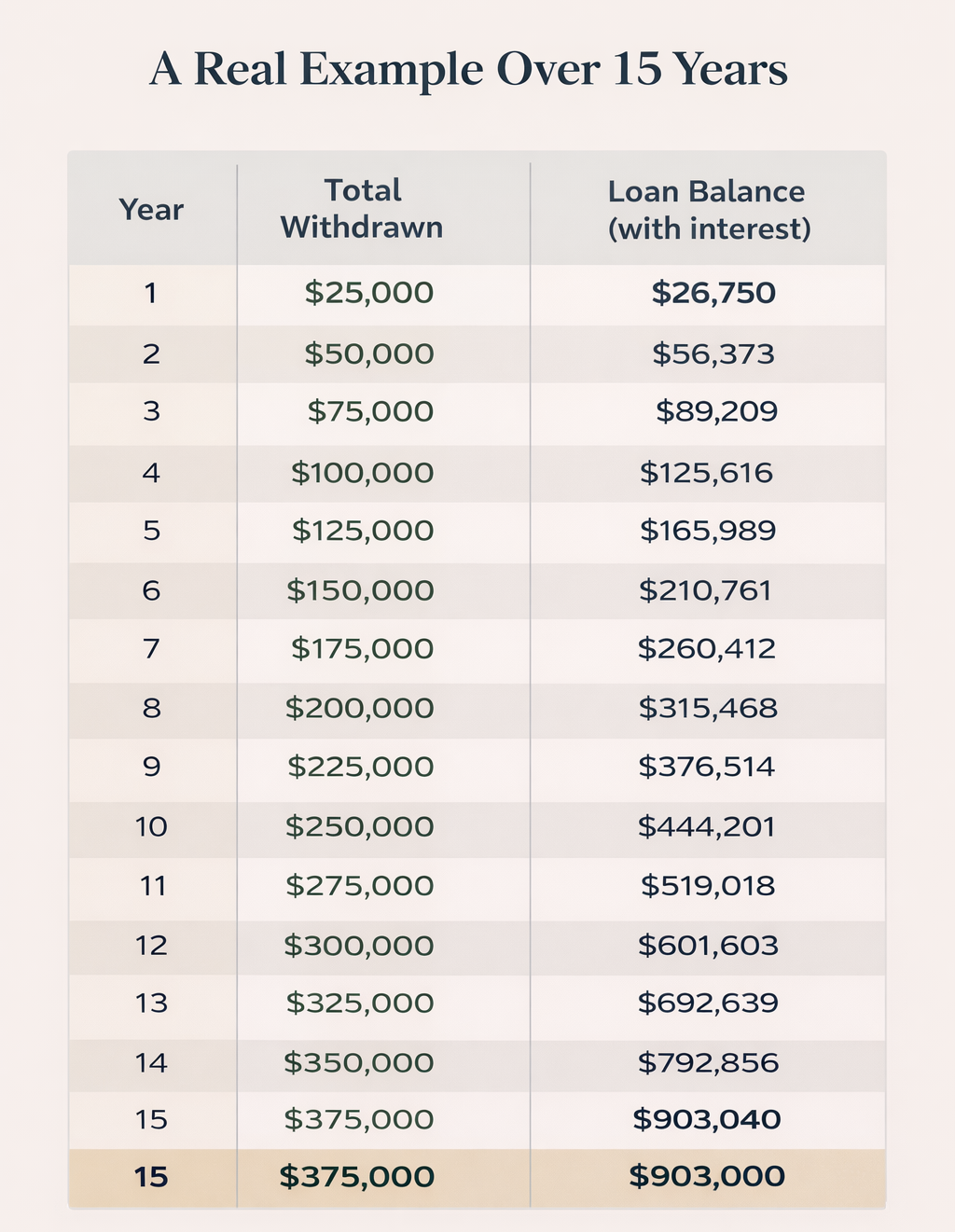

Here is an example of a reverse mortgage where an owner has $800,000 in equity and is borrowing $25,000/year at 7% interest.

After 15 years, the homeowner has received $375,000 in cash, but now owes approximately $903,000.That’s the part many people don’t expect.

What This Means for Your Equity

Because interest is being charged on both the original borrowing and the accumulated interest, the balance grows faster than most assume. In this example, the loan has actually exceeded the original $800,000 in equity. Depending on home value growth, a significant portion — or even all — of the original equity could be gone.

Your home equity is often your largest financial asset. A reverse mortgage converts that asset into usable cash, but it does so by steadily reducing what remains over time.

When It Can Make Sense

That doesn’t mean a reverse mortgage is inherently a bad option. There are situations where it might be the only available solution. If you plan to stay in your home long-term, need access to funds for living expenses or care, and don’t have strong alternative income sources, it can allow you to remain in place.

When to Be More Cautious

But it’s important to approach it with clarity. If there is a possibility you may move within a few years, if you have other financial options available, or if preserving equity for your family is important to you, then this is a decision that deserves a deeper conversation.

What Buyers and Sellers Should Know

Even for those not considering a reverse mortgage personally, it’s helpful to understand how they show up in the market. When a property is sold with a reverse mortgage in place, the loan must be repaid on closing, and the payout amount can be higher than expected due to accumulated interest. This can impact the ability of the sale to close.

What Most People Miss Before They Retire

One of the most overlooked parts of retirement planning is future access to credit. Before retiring, it’s often wise to set up a line of credit on your home while you still have qualifying income. This creates flexibility later, allowing you to access funds without needing employment income to requalify. What many people don’t realize is that a line of credit is typically tied to a mortgage. Homeowners rush to pay off their mortgage, only to find afterward that they no longer qualify for a line of credit once they’re retired. At that point, the option is gone. These are decisions that need to be structured before retirement — not after.

The Bottom Line

A reverse mortgage is a financial tool — not a solution on its own. It can work well in the right circumstances, but it is, at its core, a trade: future equity in exchange for present-day cash, and that trade deserves to be fully understood, and used as a last resort.

Final Thought

In real estate, the decisions that matter most are rarely the ones that feel urgent — they’re the ones that shape your long-term financial position. If you’re considering a reverse mortgage, take the time to ask questions and explore your options. Clarity now can prevent difficult surprises later.